CT600 vs annual accounts: what's the difference?

You filed beautiful accounts at Companies House. Your accountant emails that the CT600 is still outstanding. Same numbers, different form, different deadline, different government body.

CT600 and annual accounts are not duplicates. They answer different questions for different recipients.

What is the difference between CT600 and annual accounts?

Annual accounts are the statutory financial statements filed at Companies House. The CT600 is HMRC's company tax return that calculates corporation tax on taxable profits.

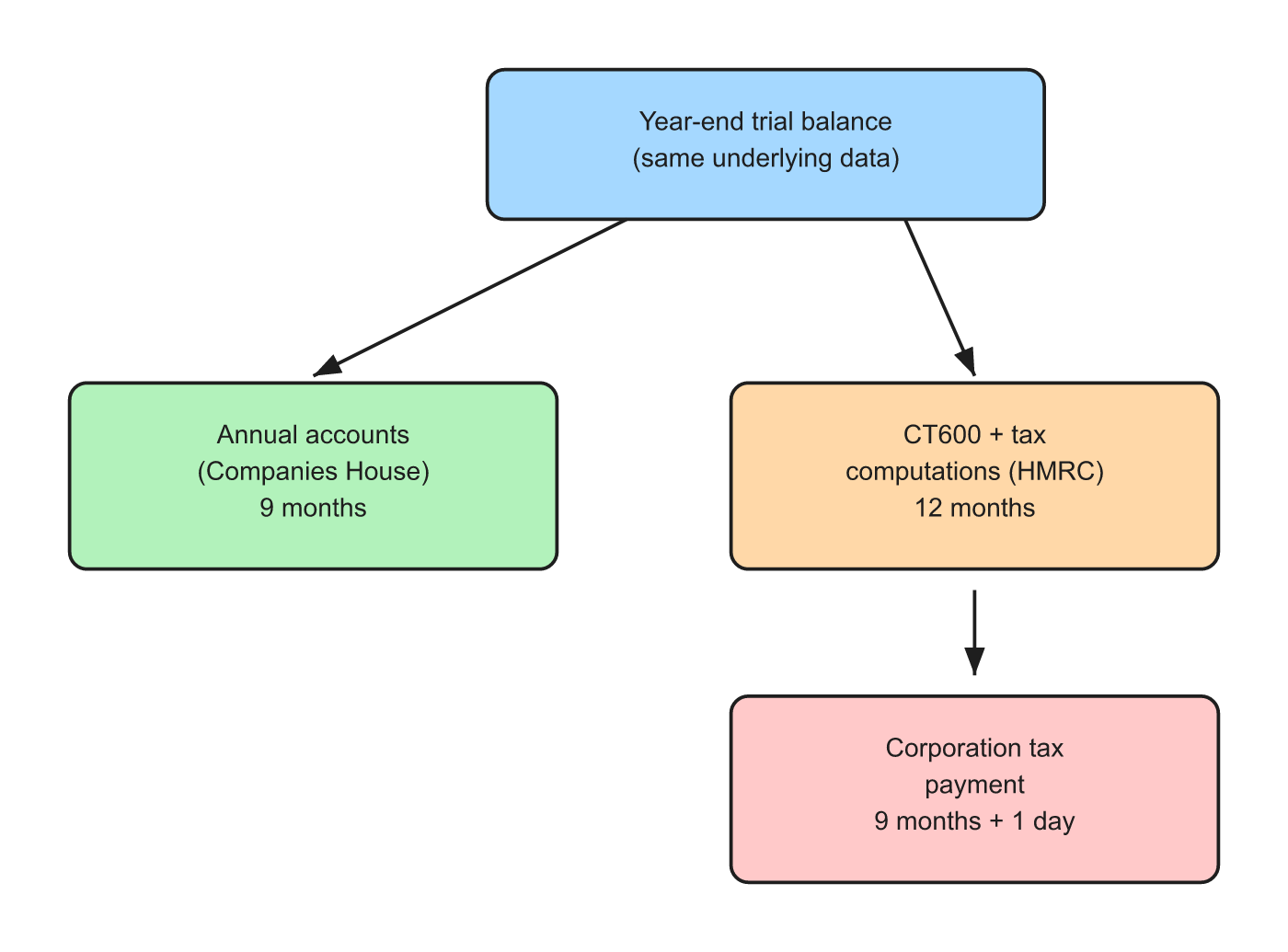

Both usually come from the same year-end trial balance. One is public disclosure. The other is tax computation.

Annual accounts | CT600 (company tax return) | |

Sent to | Companies House | HMRC |

Main purpose | Statutory accounts on public record | Report tax liability and claims |

Typical format | iXBRL accounts (abbreviated or full) | CT600 return plus tax computations |

Private Ltd deadline | 9 months after year end | Filing: 12 months after year end |

Tax payment | Not included | Corporation tax due 9 months and 1 day after year end |

For deadline examples, see CT600 filing deadline.

Two filings from one set of books

SYSTEM INSIGHT / NEXT STEP

Make the next move with clarity.

If this issue is already showing up in reporting, runway, or team decisions, the next move is usually clearer with a structured finance view.

What are annual accounts?

Annual accounts show performance and position for shareholders and the public register. For many small companies, abbreviated accounts are filed at Companies House with less detail than management sees internally.

Directors approve accounts before filing. Late filing triggers Companies House penalties.

Accounts follow accounting standards (usually FRS 102 for UK companies). They are not a tax calculation.

What is a CT600?

The CT600 is the online company tax return. It reports:

Taxable profit after tax adjustments

Corporation tax due

R&D and other reliefs claimed

Losses utilised or carried forward

HMRC may ask for supporting computations showing how accounting profit became taxable profit. Add-backs and disallowances (client entertaining, depreciation, etc.) live here, not in the Companies House narrative.

R&D claims for software startups are declared on the CT600 with a technical report. See R&D tax credits for UK software startups.

Why founders confuse them

Both relate to the same accounting period. Both are prepared after year end. Both use the same bookkeeper or accountant.

The confusion shows up in three places:

Assuming Companies House filing settles tax (it does not)

Missing corporation tax payment at 9 months and 1 day while accounts are already filed

Searching "CT600 vs annual accounts" only after HMRC chases the return

Put all three dates in your compliance calendar when you set your year end.

Do the numbers have to match?

Revenue and profit in accounts and tax computations should reconcile through agreed adjustments. They will not be identical lines because tax rules differ from accounting rules.

Example: you capitalise development costs in accounts but claim R&D enhancement in tax. The CT600 reflects tax treatment. Accounts reflect accounting policy.

Investors and HMRC both expect a clear bridge between the two.

Who prepares each filing?

Often one firm prepares both from the same ledger. Sometimes Companies House accounts are filed first and tax work follows.

Startups on Xero with clean month-end close make both filings faster. Messy books slow everything.

In practice

Treat year end as a small project: finalise ledger, draft accounts, agree tax adjustments, file at Companies House, pay corporation tax, submit CT600.

A finance partner tracks the sequence so founders are not surprised in month ten.

FAQs

Is CT600 the same as annual accounts?

No. Annual accounts go to Companies House. The CT600 goes to HMRC to report and pay corporation tax.

Which is due first, CT600 or annual accounts?

Companies House accounts are usually due before the CT600 filing deadline (9 months vs 12 months for private companies). Corporation tax payment is due at 9 months and 1 day, before the CT600 filing date.

Can I file accounts without filing a CT600?

No. Both are required for an active trading company unless HMRC has agreed otherwise in specific cases.

Do investors see my CT600?

Not automatically. Companies House accounts are public. CT600 details are between you and HMRC unless you share them in diligence.

What happens if I file accounts but not the CT600?

HMRC can charge penalties for late company tax returns and interest on unpaid tax.

**Year-end filings stacking up?** Talk to an Expert or see pricing.