Late company accounts penalties: costs, risks, and recovery steps

If your company accounts are late at Companies House, the penalty is automatic. There is no grace period for being busy. There is no investor excuse.

This guide covers what it costs, what else breaks, and how to recover without making it worse next year.

What is a late company accounts penalty?

A late company accounts penalty is a fine Companies House imposes when statutory accounts are delivered after the filing deadline. For private limited companies, accounts are usually due nine months after the accounting reference date.

This is the same underlying regime as Companies House late filing penalties. This article emphasises recovery and prevention for founders already in the penalty cycle.

Recovery steps at a glance

SYSTEM INSIGHT / NEXT STEP

Make the next move with clarity.

If this issue is already showing up in reporting, runway, or team decisions, the next move is usually clearer with a structured finance view.

Penalty costs (private companies)

How late | Penalty |

Up to 1 month | £150 |

1 to 3 months | £375 |

3 to 6 months | £750 |

More than 6 months | £1,500 |

Penalties double if accounts are late in two successive financial years.

Source: GOV.UK late filing penalties guidance.

Risks beyond the fine

Risk | Impact on startups |

Public overdue status | Visible on Companies House; diligence red flag |

Investor confidence | Boards question operational control |

Strike-off | Extreme non-compliance can threaten company status |

Director duties | Personal responsibility for timely filing |

Rejected accounts | Fixing format errors after the deadline still attracts penalties |

The penalty is the visible cost. The fundraising friction is often larger.

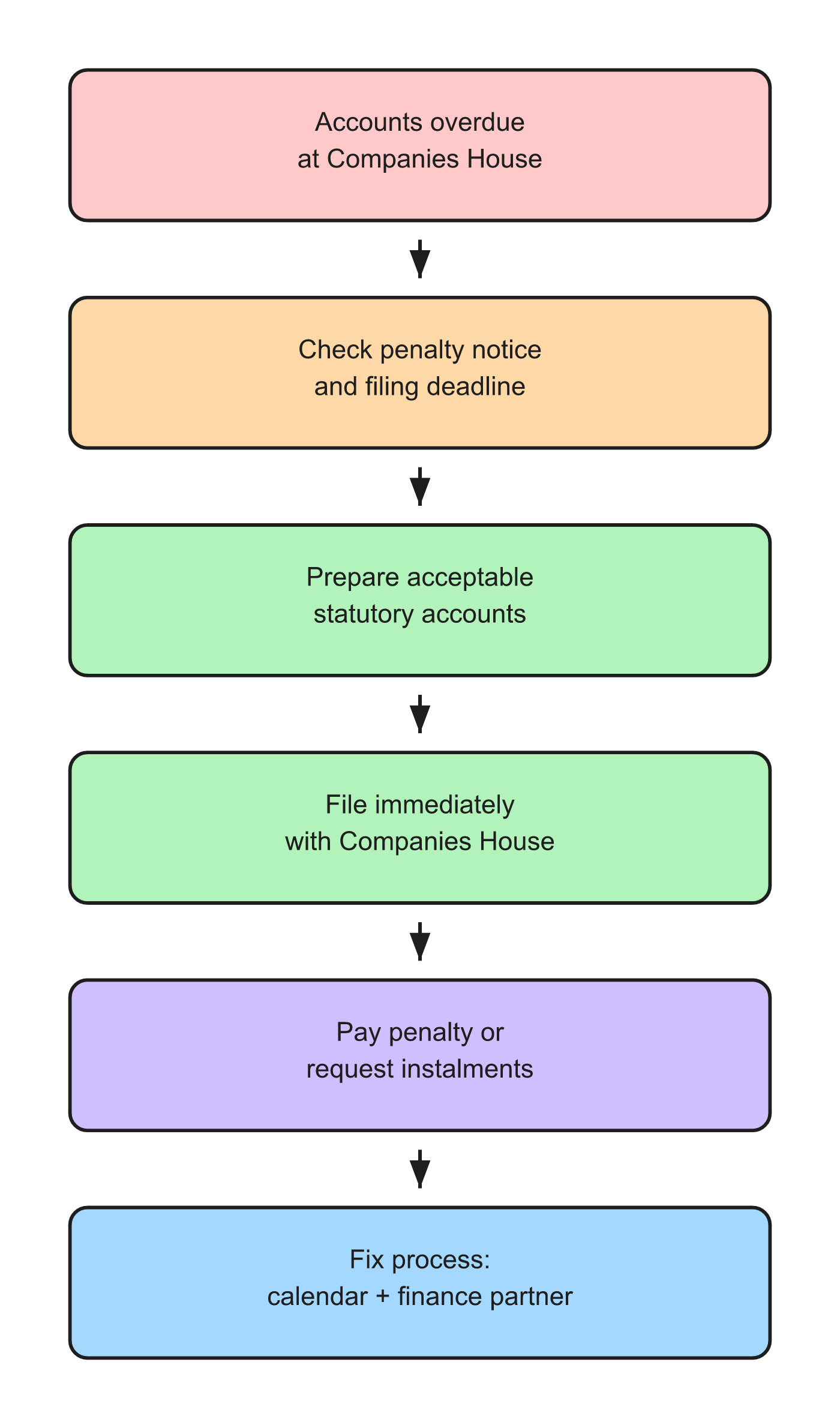

Recovery steps if accounts are already late

1. Confirm the deadline and penalty notice

Check your accounting reference date, the statutory filing date, and any penalty notice from Companies House. Do not guess from memory.

2. Prepare acceptable accounts immediately

Accounts must meet filing requirements (signed, correct format, iXBRL where required). Rejected filings that are corrected late still incur penalties.

3. File now

Every day late can move you into a higher penalty band. File before worrying about appeal.

4. Pay the penalty

Pay online via GOV.UK. If cash is tight, Companies House may accept instalments if you contact them promptly.

5. Appeal only if genuinely exceptional

Routine pressure does not qualify. Document exceptional circumstances per GOV.UK appeal guidance.

6. Fix the operating system

Register for Companies House email reminders

Align accountant deliverables to month 7 to 8 after year end, not month 9

Run monthly month-end close so year-end is assembly, not archaeology

How to prevent repeat penalties

Action | Owner |

Calendar ARD + 9-month CH deadline | Founder / CoSec |

Separate CH deadline from CT600 deadline | Finance lead |

Monthly management accounts | Finance partner |

Pre-year-end accounts prep (month 10 to 11) | Accountant |

In practice

Statutory filing works best when it sits inside monthly finance ops, not a standalone annual scramble. A finance partner calendars Companies House and HMRC dates, runs management accounts through the year, and assembles year-end from reconciled books.

FAQs

What is the penalty for filing company accounts late?

For private companies, penalties start at £150 (up to one month late) and rise to £1,500 (more than six months late).

Is a late company accounts penalty the same as a Companies House late filing penalty?

Yes. They refer to the same automatic fines for overdue statutory accounts.

Can investors see if our accounts are late?

Yes. Companies House records show filing status. Due diligence routinely checks this.

What if accounts were rejected and refiled late?

Late delivery after the deadline attracts a penalty even if the first submission was rejected for errors.

How do we avoid a second doubled penalty?

File on time for the next financial year. Two successive late years double the fine.

**Accounts overdue and need a recovery plan?** Talk to an Expert.