MTD for self-employed: records you need to keep

Your startup runs through a Ltd company, but you also invoice as a consultant or receive UK property income. HMRC's Making Tax Digital for Income Tax (MTD ITSA) rules apply to that personal income separately from company accounts.

From 6 April 2026, many self-employed people and landlords above the income threshold must keep digital records and send quarterly updates, not just file Self Assessment in January.

If you are unsure whether you are in scope, read who is affected by MTD for Income Tax first. This guide covers what to record once you are.

What digital records must self-employed people keep for MTD?

You need digital records of self-employment and UK property income and expenses. HMRC-compatible software must create, store, and correct these records, then send quarterly updates and your final declaration.

You do not need digital records for every income type. Pensions, dividends, and savings are still reported on your tax return, but may not require the same digital record trail as trading income.

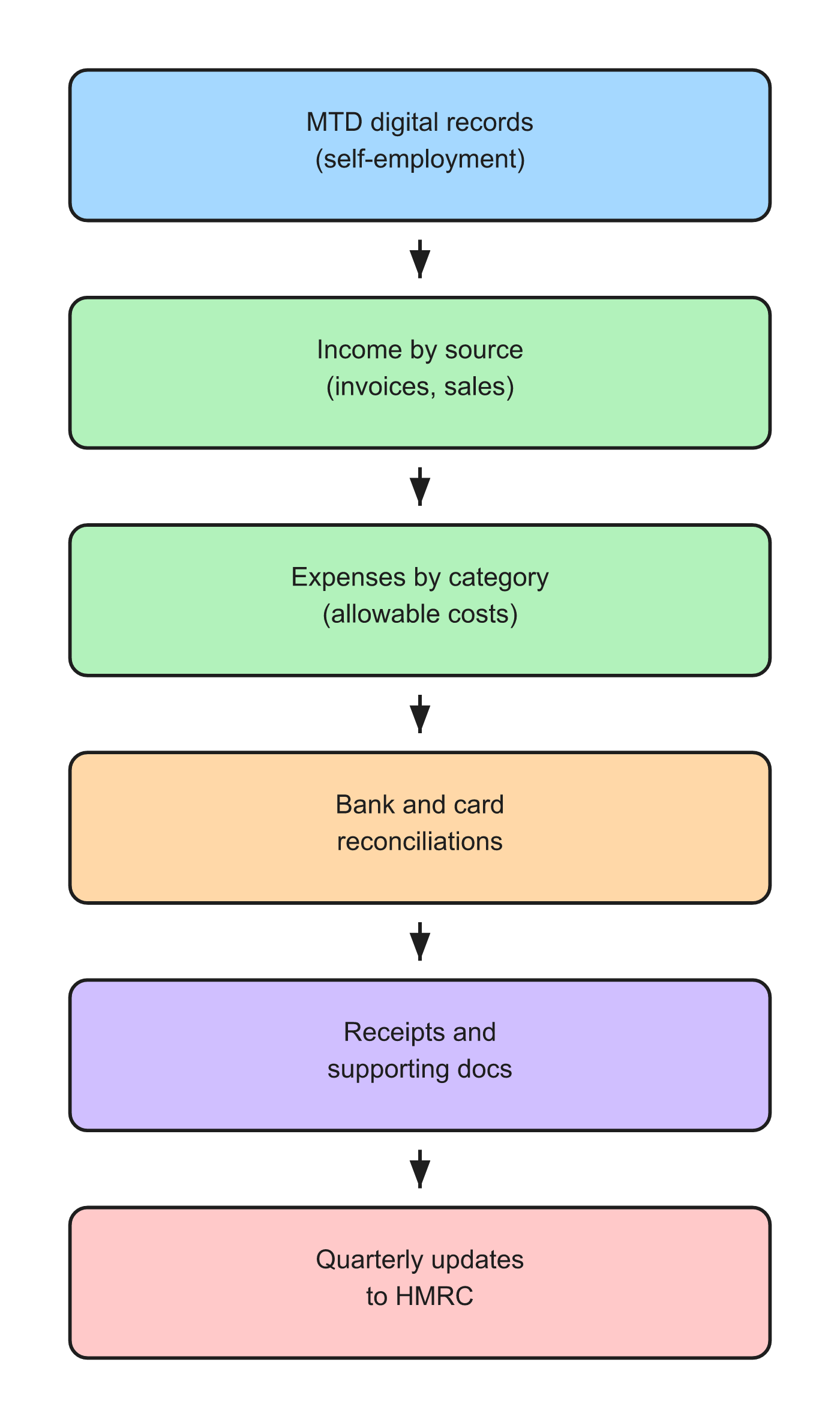

Record keeping flow for MTD ITSA

SYSTEM INSIGHT / NEXT STEP

Make the next move with clarity.

If this issue is already showing up in reporting, runway, or team decisions, the next move is usually clearer with a structured finance view.

1. Income records

Capture gross income when it is earned or received, depending on your accounting basis (cash or accruals, as allowed for your business).

Typical sources:

Sales invoices and payment confirmations

Platform payouts (marketplaces, freelance sites)

Rental income schedules for UK property

Tag income by source if you have more than one trade or property business. MTD submissions are per business, not one blended bucket.

2. Expense records

Record allowable expenses in categories HMRC recognises: travel, office costs, professional fees, equipment, and similar.

Each entry needs enough detail to defend the claim: date, amount, supplier, and business purpose. "Miscellaneous" every month is a red flag in enquiry.

Keep personal and business spend separated at bank level where possible. Mixed accounts slow down quarterly updates.

3. Bank and card reconciliations

Digital record keeping still means reconciling feeds to your ledger. Unreconciled transactions at quarter end become errors in your update.

Founders often run company books in Xero and personal trade income in a separate Xero organisation or sole trader ledger. Do not post director salary twice or confuse Ltd expenses with personal trade costs.

4. Receipts and supporting documents

MTD is digital-first, but you still need evidence. Store PDF invoices and receipts linked to transactions. Photos in a shoebox folder are not a system.

For property, keep tenancy agreements, agent statements, and repair invoices. For consulting, keep contracts and timesheets if you bill by day rate.

5. Quarterly updates (what you send HMRC)

Quarterly updates are summaries of income and expenses for the period. They are not full tax returns.

Software aggregates your digital records into the update. Late or inconsistent categorisation in month two shows up as a painful quarter four.

Calendar quarter vs tax year quarter elections matter for landlords. See MTD quarterly submissions.

6. Final declaration

After four quarterly updates, you complete a final declaration and pay balancing tax by 31 January (existing Self Assessment rhythm).

Other income (dividends from your startup, for example) is included here even if it was not part of quarterly digital records.

MTD records mistakes founders make

Using the company Xero file for personal consulting income without a clear entity split.

Waiting until January to categorise a full year. MTD expects ongoing digital hygiene.

Choosing software that handles VAT but not MTD ITSA when you need both.

Ignoring property income from a single buy-to-let while focusing on the startup day job.

In practice

Founders in scope often need two rhythms: company month-end close for the Ltd, and personal digital records for trade or property income.

A finance partner can separate entities, configure categories once, and align quarterly calendars with company VAT and payroll deadlines.

FAQs

What records do I need for Making Tax Digital if I am self-employed?

Digital records of self-employment income and allowable expenses, maintained in HMRC-compatible software, plus evidence such as invoices and bank reconciliations.

Do I need digital records for dividend income from my company?

Dividends are reported on your tax return but are not part of the self-employment digital record set described in GOV.UK MTD ITSA guidance.

Can I use spreadsheets for MTD?

You need software that creates compliant digital records and submits updates to HMRC. Spreadsheets alone usually fail the digital link requirement unless bridged by approved tools.

How often must I send MTD updates?

Four quarterly updates per year for each in-scope business, plus a final declaration.

Does MTD replace Self Assessment?

MTD changes how you keep records and report during the year. You still complete a final declaration under the MTD for Income Tax process.

**Personal trade income alongside your startup?** Talk to an Expert or see MTD services.