R&D tax credits for UK software startups: qualification guide

Your engineers ship features every sprint. HMRC does not automatically call that research and development. R&D tax relief rewards projects that tackle technological uncertainty, not routine product work.

For loss-making UK software startups, a valid claim can return cash to the business. A weak claim wastes fees and invites enquiry.

Do software startups qualify for UK R&D tax relief?

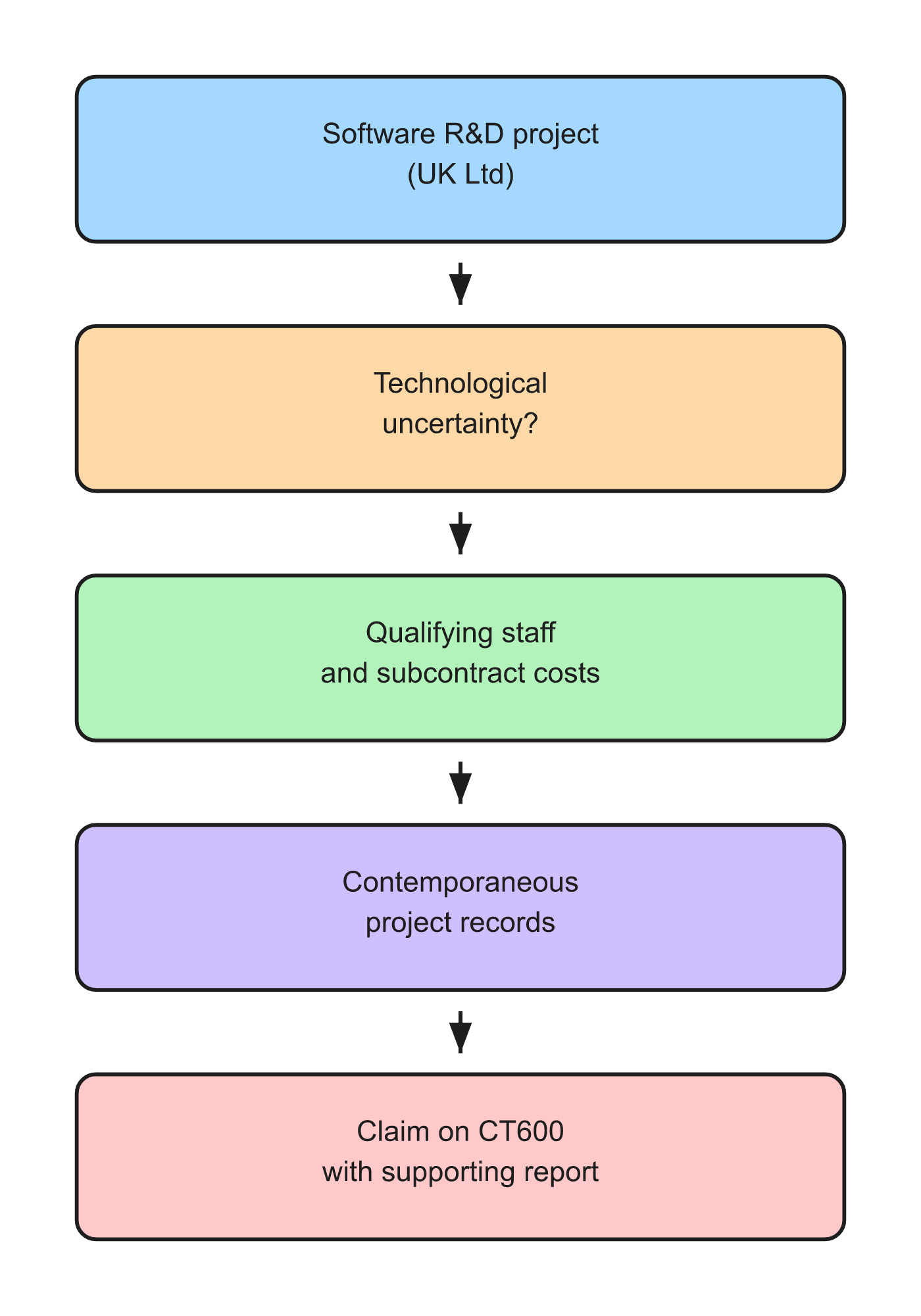

Often yes, if development work seeks an advance in science or technology and faces uncertainty that competent professionals cannot readily resolve.

Building a standard CRUD app on known frameworks is usually routine. Building novel infrastructure, algorithms, or integrations where the technical path was unclear may qualify.

Qualification is project-based, not company-based. One eligible project does not make every sprint eligible.

Qualification flow for software R&D

SYSTEM INSIGHT / NEXT STEP

Make the next move with clarity.

If this issue is already showing up in reporting, runway, or team decisions, the next move is usually clearer with a structured finance view.

What counts as technological uncertainty?

HMRC looks for uncertainty about whether something is scientifically or technologically possible, or how to achieve it in practice.

Examples that often warrant scrutiny (not automatic approval):

New performance or scale targets not met by off-the-shelf tools

Integration between systems where no established pattern existed

Security or data architecture problems without a known solution

Material algorithmic work beyond configuring existing libraries

Examples that usually fail:

UI redesigns and cosmetic front-end work

Bug fixes on existing production code without a wider advance

Choosing between well-documented frameworks

DevOps setup using standard cloud patterns

Write the uncertainty in plain language at the time work happens, not in hindsight at year end.

Eligible costs (typical for software)

Qualifying expenditure often includes:

Staff salaries and employer costs for those doing eligible R&D

Subcontractor costs (subject to rules and caps)

Software licences used directly in R&D

Cloud compute for eligible development environments (case by case)

Not every engineering salary qualifies. Apportion time to eligible projects. "Everyone is R&D" is not credible.

Rates and schemes changed from 1 April 2024. Loss-making R&D-intensive SMEs may access enhanced relief under current rules. Confirm rates and scheme eligibility with your adviser before modelling cash impact.

Documentation HMRC expects

Claims need contemporaneous evidence:

Project charters or specs describing the technical challenge

Sprint notes, architecture diagrams, failed experiments

Time records or reasonable apportionment methodology

Git history supporting when work occurred

Reconstructing a claim from memory in March for a December year end is how startups lose enquiries.

Align project codes in Jira (or similar) with R&D narratives early.

How the claim hits the CT600

R&D relief is claimed through the company tax return. Enhanced expenditure reduces taxable profit or generates a payable credit depending on your position.

The CT600 is filed with HMRC, separate from Companies House accounts. A technical report usually accompanies first claims and material increases.

File on time. Late CT600 delays refunds and signals poor compliance in diligence.

Common software startup mistakes

Claiming all engineering payroll because the product is "innovative".

No paper trail linking sprints to uncertainty.

Mixing capitalised product development in accounts with R&D narratives without a clear bridge.

Using a template narrative copied from another startup.

Ignoring subcontractor and overseas developer rules.

In practice

Treat R&D tracking as a monthly habit: tag projects, capture uncertainty statements, and review eligible spend with your accountant before year end.

Finance ops that already run clean month-end close make apportionment and payroll splits faster.

FAQs

Can a SaaS startup claim R&D tax credits?

Yes, if specific projects meet HMRC's technological uncertainty tests. Routine SaaS feature work alone is usually insufficient.

What costs qualify for R&D tax relief in software?

Often qualifying staff costs, eligible subcontractor costs, and some software or cloud costs tied to eligible projects. Rules vary by scheme and period.

How is R&D claimed in the UK?

Through the company tax return (CT600) with computations and usually a technical report supporting the claim.

Do I need an R&D specialist?

Complex claims benefit from specialists. Simple first claims still need competent tax advice and good documentation.

When should we start documenting R&D?

When the project starts, not at year end.

**Building a software R&D claim with clean payroll and project records?** Talk to an Expert or see pricing.